Q3 2020 Finance Trends Demonstrate Automotive Industry’s Resilience

As we look at the market in Q3, there were a number of notable statistics that can help lenders identify trends and inform strategy.

As we look at the market in Q3, there were a number of notable statistics that can help lenders identify trends and inform strategy.

IMAGE: Experian

As the third quarter of 2020 ended, it also marked eight months of the COVID-19 pandemic. It’s had an undeniable impact on the automotive industry, but much like previous downturns, the industry remains resilient. That said, there are many ways in which the pandemic is unique compared to other significant events. As a result, it’s difficult to try and forecast outcomes by looking at historical data. Instead, lenders should pay attention to current data and trends to inform the most strategic decisions.

Lenders should continue to pay close attention to how trends develop over the next few quarters to ensure they are making strategic decisions.

As we look at the automotive finance market in Q3 2020, there were a number of notable statistics that can help lenders identify trends and inform strategy, including subprime originations at record lows, leasing coming closer to expected levels, prime consumers shifting back to used vehicles, and delinquency rates seeing year-over-year drops. Here’s a breakdown of why these trends matter.

Subprime Originations Reach Historic Lows

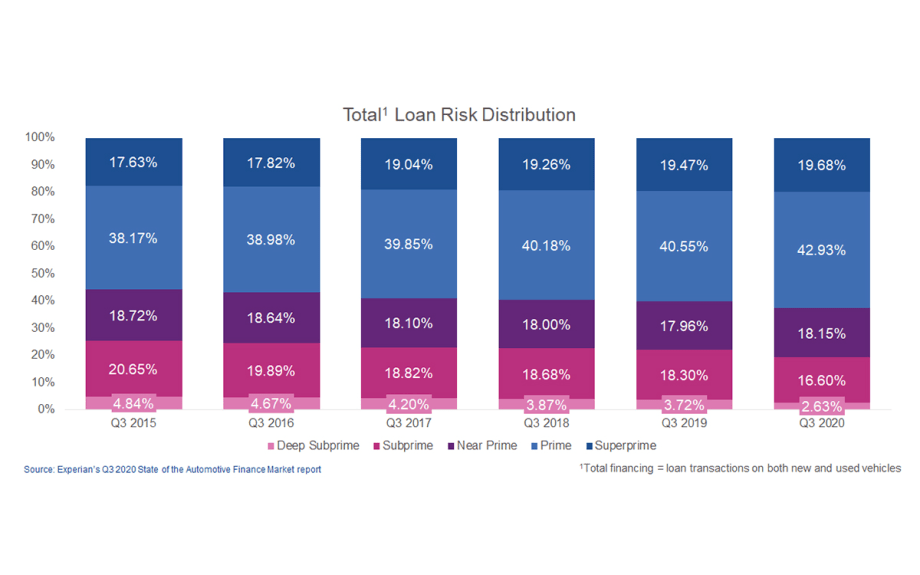

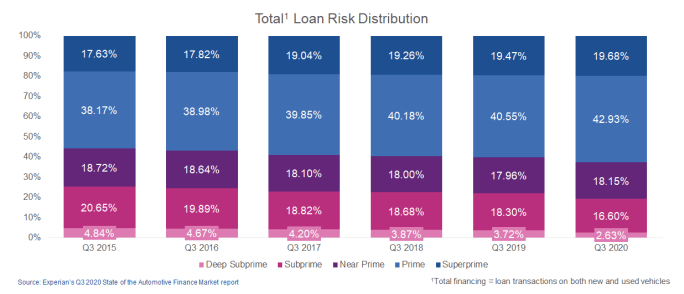

Over the last five years, we’ve seen subprime originations continually decline, and that continued in Q3 2020. Subprime loans represented 19.23% of originations in Q3 2020, compared to 22.02% in Q3 2019. Some point to COVID-19 as the singular reason for the year-over-year decline, and while it no doubt had an impact, it’s likely a combination of factors. Taking a step back and looking at the ongoing trends, the decline in subprime originations dates all the way back to 2015, when we saw subprime comprise 25.49% of loans, and decrease since then.

Figure 1: Deep subprime loans remain under 3% and reaches record low.

IMAGE: Experian

COVID-19 has had the most dramatic impact on the subprime segment, with volumes shrinking more than in other segments. This could be due to subprime consumers simply not being in market for a vehicle, with rising unemployment rates as a result of the pandemic. Another reason for the drop in overall volume being down for the subprime market could be improved credit quality. The average credit score for a new vehicle loan has increased 15 points in the last five years: from 718 in Q3 2015 to 733 in Q3 2020. On the used vehicle side, the average credit score has increased 12 points in the same time frame, from 653 in Q3 2015 to 665 in Q3 2020.

Leasing Comes Closer to Expected Levels

Leasing comprised 26.2% of new vehicles in Q3 2020. While this is down year-over-year — it was 30.27% in Q3 2019 — we’re seeing leasing rebound from the initial impact of COVID-19. In the early days of the pandemic, there was a sudden drop in leasing, likely due to a few factors. With stay at home orders, some consumers couldn’t get to the dealership to return their lease, while others who traditionally lease were drawn back into the loan space by heavy incentive offers. Despite being down year-over-year, it appears that consumers are returning to historical patterns, with leasing coming closer to the 30% mark, where it’s hovered since Q4 2015. This is important because leases play a large role in the availability of late-model used vehicles.

Used Vehicles Regain Popularity for Prime Consumers

Another area where we are seeing consumers return to historic patterns is in the used vehicle space. Due to strong incentives, more prime consumers opted for new vehicles in the second quarter of 2020, reversing a trend of prime and super prime consumers selecting late-model used vehicles, which had been ongoing for a few quarters. With fewer incentives available in Q3 2020, increased percentages of prime and super prime consumers returned to purchasing used vehicles. In total, super prime and prime consumers comprised 55.3% of used vehicle lending in Q3 2020 — a record high.

Delinquencies Decrease Year-Over-Year

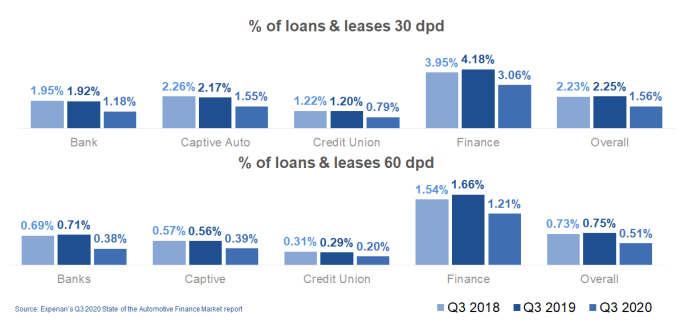

Delinquencies are often looked to as a health barometer for the automotive industry, and in Q3 2020, the data showed positive trends. Thirty-day delinquencies dropped year-over-year, from 2.25% in Q3 2019 to 1.56% in Q3 2020, while 60-day delinquencies also saw a decrease, from 0.75% in Q3 2019 to 0.51% in Q3 2020.

Figure 2: Percentage of loans and leases that are delinquent decreased as accommodation programs remain an impact.

IMAGE: Experian

The decline in 30- and 60-day delinquency rates is a notable trend for the industry, particularly with some lender accommodation programs coming to an end. We need to consider the impact these programs have had on consumers. For example, some consumers likely leveraged financial assistance programs to manage through hardship. With that in mind, lenders should keep a close eye on how delinquency rates evolve.

Overall, the automotive finance market continued at a steady pace. Lenders should continue to pay close attention to how trends develop over the next few quarters to ensure they are making strategic decisions. This will help keep the automotive industry, and the country, moving forward toward economic recovery.

Melinda Zabritski is Experian’s senior director of automotive financial solutions.

Originally posted on Auto Dealer Today

More F&I

Four-Figure Loan Payments on the Rise

A LendingTree analysis found that location, age and credit score play a role in the rising amount of auto loan borrowers who make monthly payments of $1,000 or more.

Read More →

APCO Holdings Acquires Fidelity Dealer Services

The finance-and-insurance product provider says the addition strengthens EasyCare’s reach across key markets.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

Ensure Your Clients Are Sure About Reinsurance

Industry experts recently broke down the complicated profit center at Agent Summit. Learn what’s relevant and what’s new to share with your dealers.

Read More →

Car Loans More Plentiful

May access opens up, as risk segments figured largely in the increased availability, Cox Automotive reported.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →

New-Vehicle Financing Hits Record

Consumers are seeking ways to make financing new-vehicle purchases manageable, from extended loan terms to smaller down payments, according to Edmunds.

Read More →

Survey Reveals What Won't Fix What's Breaking Car Sales

AutoPayPlus says extra-long auto loans are trapping consumers and threatening the dealer trade-in cycle, and that the industry is leveraging the wrong tools to combat high MSRPs.

Read More →