Recent Vintage Loans Perform Well Even as More Non-Prime Consumers Secured Credit in Second Half of 2021

With consumer credit performance maintaining healthy levels across auto, credit card, personal loans and mortgages, lenders continued to ramp up new account origination growth in the non-prime segment of the market near the end of 2021.

With consumer credit performance maintaining healthy levels across auto, credit card, personal loans and mortgages, lenders continued to ramp up new account origination growth in the non-prime segment of the market near the end of 2021.

TRANSUNION –With consumer credit performance maintaining healthy levels across auto, credit card, personal loans and mortgages, lenders continued to ramp up new account origination growth in the non-prime segment of the market near the end of 2021. TransUnion’s (NYSE: TRU) newly released Q4 2021 Quarterly Credit Industry Insights Report (CIIR) also found that loans to non-prime borrowers increased while accounts originated during the pandemic in 2020 continued to perform as well or better when compared to loans from previous years.

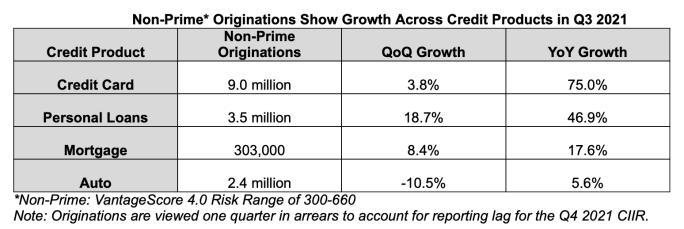

The credit card market, in particular, saw a very high rate of new account growth in Q3 2021 (latest data available) with a record 20.1 million originations, 9.0 million of which were to non-prime consumers. Overall card originations in the quarter grew 63% year-over-year, while non-prime originations increased 75% YoY from the 5.1 million non-prime originations that occurred in Q3 2020. The non-prime risk range includes the subprime risk tier (defined as a VantageScore 4.0 range of 300-600) as well as the near prime risk tier (score range of 600-660).

“There was a great deal of uncertainty in the initial months of the pandemic, and many lenders opted to take a wait and see approach. Adding to the uncertainty was the jump in consumers in loan accommodation programs, and questions on how those consumers would perform once they exited those programs. Lending to below prime consumers was suppressed and financial institutions turned their focus to the prime areas of the market to help mitigate risk,” said Charlie Wise, senior vice president of research and consulting at TransUnion. “Toward the end of 2021, the majority of accommodation programs have expired and lenders have seen that consumers continue to perform well on their credit obligations. Lenders are eager to pursue growth, including expanding back into the non-prime consumer segment.”

Supply issues have impacted sales volume in the auto industry and consequently, auto originations have stayed relatively flat. However, overall originations were buoyed by the below prime segment – which grew from 2.3 million in Q3 2020 to 2.4 million in Q3 2021. The mortgage industry, on the other hand, saw explosive growth throughout the pandemic with high levels of originations several quarters in a row due to the low interest rate environment. While non-prime consumers account for a fraction of all originations, the non-prime risk segment has also seen recent growth, with an increase of 17.6% YoY in Q3 2021, despite overall originations falling -12.6% in that same period.

Despite recent upticks in delinquencies in the most recent quarter, serious delinquency rates also remained near or below pre-pandemic levels in the wake of expired forbearance programs, which has continued to restore lender confidence. Borrower-level 60+ days past due (DPD) delinquencies for personal loans saw a seasonal uptick in Q4 2021 to 3.00%, but still remains well below the 3.48% observed in Q4 2019. The borrower-level 90+DPD for credit card reflects a similar trend and reached 1.48% in Q4 2021, but remains well below the 2.19% delinquency rate in Q4 2019.

TransUnion also looked at the 12-month performance of loans originated in 2020 compared to earlier years to better gauge consumer credit health. All credit products either outperformed or had similar performance compared to accounts opened in 2018 and 2019.

“As the economy continues to recover and consumer credit health remains strong, lenders will likely continue to extend access to credit across the risk spectrum, including non-prime consumers, and origination volumes are expected to grow. Credit growth is also likely to be bolstered as consumers return to credit markets in the wake of government stimulus programs during the pandemic, which injected excess liquidity into the consumer wallets. As this excess liquidity wanes, we expect to see consumer credit demand return to more normal patterns,” added Wise.

For more information about the report, please register for the Q4 2021 Quarterly Credit Industry Insights Report Webinar.

More F&I

Affordability Shapes Auto Demand

Auto originations increased 1% in the first quarter, and electric vehicles are rebounding, according to TransUnion's latest credit report.

Read More →

The Evolution of Agency Development in Modern F&I

General agents have a different roadmap for success than their predecessors. It will pay for them to follow it in order to be true dealer partners.

Read More →

Four-Figure Loan Payments on the Rise

A LendingTree analysis found that location, age and credit score play a role in the rising amount of auto loan borrowers who make monthly payments of $1,000 or more.

Read More →

APCO Holdings Acquires Fidelity Dealer Services

The finance-and-insurance product provider says the addition strengthens EasyCare’s reach across key markets.

Read More →

Tariffs Could Raise Insurance Premiums

As U.S. import tariffs affect repair costs, consumers might find it more affordable to replace a damaged vehicle, according to recent Insurify tariff analysis.

Read More →

Smaller Loans, Longer Terms

The youngest generation of car buyers is more likely to finance less expensive vehicles, more than half of generation Z consumers borrowing less than $25,000.

Read More →

Ensure Your Clients Are Sure About Reinsurance

Industry experts recently broke down the complicated profit center at Agent Summit. Learn what’s relevant and what’s new to share with your dealers.

Read More →

Car Loans More Plentiful

May access opens up, as risk segments figured largely in the increased availability, Cox Automotive reported.

Read More →

First-Quarter Sees Long Auto Loan Growth

Experian data show more consumers are tapping the method, along with refinancings, to afford buying. Meanwhile, subprime borrowers are getting more access.

Read More →

Auto Consumer Anxiety Presents Opportunity

A survey of U.S. drivers found the majority are concerned about finances and the economy, but those fears make many ready to buy vehicle-protection products.

Read More →