The FTC Suggests We Buckle Up

The FTC recently issued a report that summarizes its enforcement actions, roundtable findings, consumer workshops, and in-person interviews with 38 Washington D.C. metro-area consumers focused on deceptive advertising practices, spot-delivery, and voluntary protection products.

The FTC recently issued a report that summarizes its enforcement actions, roundtable findings, consumer workshops, and in-person interviews with 38 Washington D.C. metro-area consumers focused on deceptive advertising practices, spot-delivery, and voluntary protection products.

IMAGE: Lumi Nola via GettyImages.com

The Federal Trade Commission (FTC) maintains a blog on its website intended to assist businesses with their compliance efforts.(www.ftc.gov/tips-advice/business-center). Currently there are 96 blog posts for the automobile industry. I periodically review the blog posting to keep up with FTC thinking on compliance issues. I recently came across a blog titled “Buckle Up: Navigating Auto Sales and Financing.” I’m not sure if the report writers are just making a play on the seat belt for safety analogy or if the feds are blasting a warning shot to the industry to get ready for potential investigations and enforcement actions.

Like most dealers and agents, we have been recommending transparency in the sales and F&I processes for the nearly two decades.

This report summarizes FTC enforcement actions, roundtable findings, consumer workshops, and in-person interviews with 38 Washington D.C. metro-area consumers focused on deceptive advertising practices, spot-delivery, and voluntary protection products (VPP).

It is important to pay attention to the report’s findings instead of dismissing them. The FTC is the primary agency responsible for automotive industry oversight. Understand that if it initiates an investigation into a dealer’s sales and finance practices, it will likely have this viewpoint of industry best practices and use it as the standard to measure the dealer’s compliance.

It is equally important to remember that with one exception to the agency’s findings, we address many of these issues, along with solutions, when we design and implement a compliance management system (CMS). Dealers often look to their VPP provider to assist with solutions.

The report focused on six components in the sale and financing of a vehicle: advertising, price and financing terms negotiations, VPP; document execution, and renegotiations.

Auto Advertising

The FTC reported that many consumers interviewed are attracted by dealer advertisements that offer low prices, incentives, or 0% APR, but many are told that the offers would not apply to their transaction too late in the process.

While “Buckle Up” does not offer solutions to all its findings, the FTC does remind that “dealers should make only accurate and non-misleading advertising claims to consumers, advertise terms that are actually available, and clearly and conspicuously disclose material qualifications or limitations on any advertised deal.”

A dealership should have its advertising periodically reviewed to confirm it adheres to the FTC’s reminder, as well as Truth in Lending Act (TILA) disclosures if a trigger term is advertised.

Negotiating a Price

Several desking practices were presented as confusing in the study. Some expressed confusion about how the price they were offered depended on rebates or other offers. Others purchased a vehicle for the sticker price without negotiating because they felt the quoted price was fixed. Still others bristled at the practice of focusing solely on the monthly payment, feeling it was an attempt to hide the vehicle price. Finally some consumers expressed confusion when the dealer used a tablet to digitally present price and financing options. They felt the dealer tended to scroll to the bottom of the document for a signature without adequately reviewing the options.

The FTC’s recommendation to provide pricing transparency: “Given the length and complexity of auto sales and financing transactions, discussing the ‘out-the-door’ price of the vehicle (the total price, before financing, including taxes and fees) beforediscussing financing could help avoid confusion.”

This would suggest that the first pencil be an out-the-door quote, then start with financing options on the second pencil. Not sure that I would push this recommendation. Instead, you should find an e-pencil provider for your dealer. Ensure that every pencil include all the components of the out-the-door number. Also, avoid reducing the cash price by the amount of a potential rebate without disclosing the amount of the rebate.

Negotiating Financing Terms

The FTC comingles findings from both the sales and financing process in this portion of its report. Some consumers interviewed expressed confusion over terms promised by the salesperson that were reversed in the finance office. Others did not recall clear financing terms during the sales process, including term and APR.

The FTC’s viewpoint: “In financing negotiations, dealers should honor discounts or other terms sales personnel promise consumers, or sales personnel should not promise them. If there are limitations on the discounts or terms being offered, dealership representatives, whether on the sales floor or in the financing office, should explain those limitations clearly and consistently.”

We recommend a clear final pencil with price and financing terms, followed by a menu presentation with the same terms. Many of our clients have the consumer initial the menu base payment to affirm the consumer’s acknowledgement of payment without VPP options.

Ancillary Products and Services

We call these products voluntary protection products. The FTC continue to label them as add-ons.

The report states that “Most study participants’ contracts included charges for add-ons, but the interviews revealed consumers who were unaware which add-ons they had purchased, were unable to identify add-ons in the paperwork, were unclear what those add-ons included, and sometimes did not realize they had purchased any add-ons at all. Indeed, add-ons were the single greatest area of confusion observed in the study.”

There were six specific issues related to VPP sales noted in the report:

Late, limited, or no discussion of add-ons: The FTC seems to infer that the discussion or presentation of VPP should come earlier in the process, by the sales staff.

Confusion about whether add-ons are free: Some participants thought that the VPP were included in the deal at no additional charge. This finding would suggest the solution would be to avoid discussion during the sales process, contrary to its conclusion on late, limited, or no discussion of VPP.

Impressions that add-ons are mandatory: One participant said her dealer told her GAP was a mandatory purchase to get financing. I’ve observed the same from viewing videos or reviewing paperwork in the file. If any VPP is required for financing, its cost must be included in the consumer’s APR and finance charge TILA disclosures.

Unexpected limitations of add-on products: Some participants purchased vehicle service plans and were later surprised to learn they had to pay for uncovered repairs or services.

Opaque pricing of add-ons: Some of the study participants said that the finance manager only disclosed the monthly payment effect when presenting products or indicated they were told that the add-on cost would roll into their financing or that it was already included in the price of the vehicle.

Bundling add-ons: One consumer reported that she wanted a specific product out of a bundled product but had to take the package instead of the one she wanted. Another consumer had issues verifying the discount when purchasing a bundled package.

Provided your dealer has implemented clear and transparent desking and menu processes, your dealers’ customers should not report any of these issues. These processes should include an e-pencil process that clearly discloses the components of the out-the-door number and the term and APR used to calculate the payment quotes.

The menu base payment should be initialed after memorializing the sales figures, ensuring the prices of selected products is clearly disclosed, and the customer signs near the final agreed upon terms.

There are additional disclosures that we recommend be included on every menu. These include that the purchase of products is optional, will not affect the customer’s APR, can be purchased separately, and is not required to obtain financing. Review the menu you either provide or recommend to your dealer to confirm these four disclosures are present and conspicuous.

You should also stress the four-disclosure rule we live by with the paper or digital trail approach to disclosures. The products selected and the agreed upon price must be disclosed and consistent on four documents: menu, buyer’s order (pre-contract disclosure in California), retail installment sales contract, and VPP registration form.

Reviewing and Signing the Documents

Some of the manufacturers’ CSI surveys ask the consumer about the amount of time spent in the F&I office. This encouraged many dealers to engage in a process improvement initiative to reduce the amount of time it takes a consumer to sell and finance a vehicle.

Many try to put a time limit on the F&I close to improve a CSI score. While I have not reviewed all the manufacturers’ CSI surveys, the ones I have discuss “time spent in the F&I office.” Some perceive this to mean a shorter amount of time. This can lead to a rushed experience.

We also do not know if these were prime or sub-prime customers, which can play a factor in time to complete a transaction. Among the concerns noted in the report:

Long, complextransaction: Many participants noted that the overall vehicle purchase transaction could last from several hours to 11 weeks and they felt overwhelmed or “just ready to sign the paper and get out” of the dealership.

Despite length of transaction, review is rushed: Some participants felt rushed when it came to paperwork signing time.

Information overload: Consumers are asked at least 80 times to sign required or best practices disclosures. This leads some to feel overwhelmed, the paperwork was too complex, and that there was it much fine print.

Electronic document review: As we continue to migrate from pulp and analog processes to electrons and digital processes, this last FTC finding is somewhat concerning. The consumers that received the transactional information via a tablet reported having trouble following along. Others reported not given adequate time to review the document as the finance manager just scrolled through it and said, “sign here.” The few consumers who received their documents on a flash drive appeared to like the lack of paper documents.

Misapprehension that deal is non-binding: There appeared to be some confusion by one participant between signing to confirm interest and signing a contract. Other participants had incorrect pre-conceived notion or impressions that big-ticket items had a cooling off period but complained that the dealer did not read his mind and correct his misunderstanding.

The FTC stayed silent on recommendations.

The irony can’t be lost that much of the disclosures that lead to information overload and length of transaction are the result of dealers’ attempts to mitigate burgeoning Dark Side laws, statutes, regulatory oversight, and litigation.

Our recommendation is that agents provide training of the proper disclosures, allowing the consumer time to review the documents if they choose to do so, and slow down.

I once attended a week-long training conducted by a larger agency. We spent at least three hours learning how to mirror the pace of the F&I close to the customer’s pace, not the F&I manager’s pace. Perhaps the consumer who feels rushed but spent less than the amount of time dictated by the dealership’s time standard would still give a less that perfect response on the CSI survey.

Renegotiation of Financing

This section of the report deals exclusively with spot delivery and yo-yo transactions. While spot deliveries are not permissible in some states, other states have clear seller’s right to cancel provisions in contract language.

The FTC’s recommendation? “Dealers should explain spot delivery to consumers before having them sign spot delivery forms. Moreover, when a consumer is called back to the dealer because their financing fall through, dealers should never use deceptive or unfair tactics to pressure the consumer into a new deal, and dealers should prepare, maintain, and provide to the consumers records documenting any changes to the deal and the reasons for the changes. It is important for consumers to know that they do not have to agree to any changes or new paperwork they are being asked to sign.”

Quite frankly, I couldn’t have put it any better.

Like most dealers and agents, we have been recommending transparency in the sales and F&I processes for the nearly two decades and providing compliance consulting and training. This FTC report affirms that consumers and the Dark Side expect the same.

Finally, there is an undercurrent of findings regarding digital information delivery. We must continue to train our dealers to review the documents, so the consumer understands what she is being asked to agree to, whether the information is delivered digitally or in paper format.

Stay safe, Good luck and, Good selling!

Gil Van Over is the executive director of Automotive Compliance Education (ACE). He is also the founder and president of gvo3 & Associates.

More Industry

Pennsylvania Dealership Under New Retailers

The sale of the Chrysler Dodge Jeep Ram store puts a family auto group on a leaner path as first-time dealers take the helm.

Read More →

Battery Storage Takes Priority Over EVs

U.S. automakers are prioritizing battery energy stationary storage over electric-vehicle production as the consumer demand for EVs lags the rest of the world.

Read More →

Auto Dealers Feel Better But Not Great

A second-quarter Cox Automotive poll of franchised retailers and independents found better views of the current market after a good spring but anticipation of third-quarter storminess.

Read More →

New-Vehicle Sales Picture Relative

A May forecast is complicated by last spring’s trade tariff effects on auto retail. Despite continued hard realities, many consumers took advantage of ways to bite the bullet.

Read More →Auto Group Acquires Third Nissan Rooftop

Iowa-based Coleman Automotive Group recently acquired its seventh dealership, McGrath Nissan, which it renamed Nissan of Elgin.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Building an Extraordinary F&I Agency

Work to determine your specialized talent, because that fact will determine everything about your agency’s future.

Read More →

Recipe for Compliance

The secret to both amazing barbecue and compliance is the same: understanding the basics and committing to a process.

Read More →

EVs Getting More Attractive

A growing percentage of U.S. consumers are open to switching and fewer are adverse to the idea, according to a recently completed survey. That’s despite the end of a tax break.

Read More →

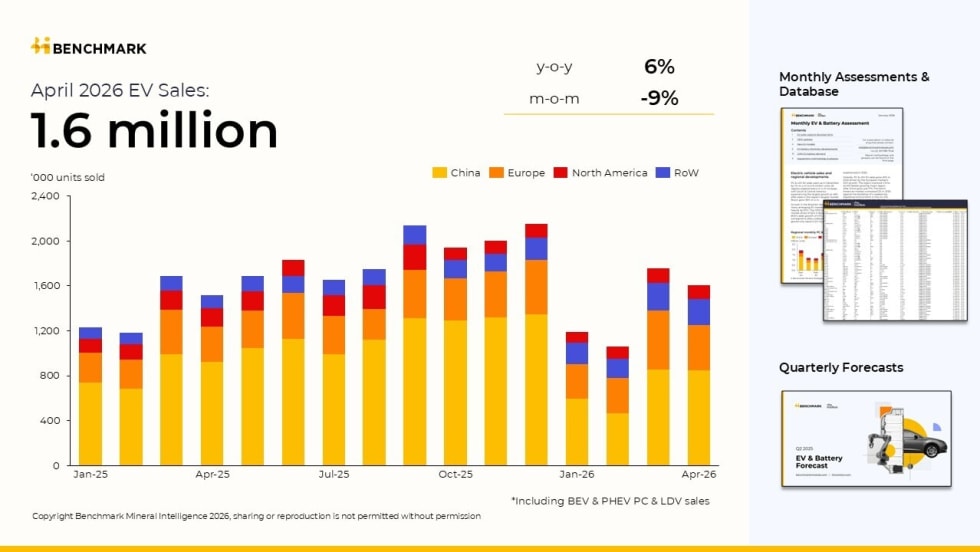

EV Sales Drop in April Following Surge

North American electric-vehicle sales were down 28% year-over-year, a sharp contrast from global EV sales growth of 6%.

Read More →