In today’s marketplace, dealer participation in reinsurance programs is becoming more popular than ever. And General Agents are coming up with more and more creative programs to meet the demand. Even smaller dealers are asking their agents to get them into those “back-end” programs that promise huge storehouses of wealth to be cashed in at some future date.

However, no matter how attractive the structure of the reinsurance program may be, the agent still has to figure out how to make the program deliver the results the dealer expects. Over the last several years, the dealers who use our process have had well above average success with these programs, so I often get inquiries asking what our secret is to making them work.

Ad Loading...

And I’ll share our “secret” in a moment.

But first, for those readers who may not be familiar with what I am talking about, what is reinsurance?

Many F&I products involve a risk of future claims. Certainly credit life and disability insurance pays claims if there is a loss to the customer. And service contracts have a risk of the insurer or administrator having to pay for future repairs. Even chemical and theft products have a risk component that involves insuring against future claims.

To pay for future claims, insurance companies and administrators put aside a substantial portion of the premiums collected from the customer. That money is referred to as "reserves." Those reserves are stashed away and collect investment income and build just like any other investment.

Once a policy has expired or the term of the risk has ended, whatever money is left over, after all claims and administration costs are paid, is considered reserve and becomes profit to the insurer. The difference between what is put into reserves and the amount paid out in claims is referred to as the "loss ratio." Obviously, the key to making a profit is to control the loss ratio so that the insurer is not paying out more in claims than they have stored away in reserves.

Ad Loading...

Here's where the dealer gets involved. In order to get new accounts and write more policies, many insurers and service contract companies have offered dealers an opportunity to participate in the potential profit from the reserves that the F&I products generate. The premiums are collected when the dealer sells a product and remitted to the insurer as usual.

However, in a reinsurance program, the insurer sets up an account for the dealers' "book of business." The insurer or administrator takes a fee for administration, usually a fee to pay for another insurance policy to protect the dealer from having losses beyond their reserves, and if there is any money left when the policy elapses, it goes to the dealer. This is set up as a separate account with stock values, etc. These deals get very complicated with A and B shares, onshore or offshore accounts, analyzing cession statements, etc.

However, the intricate details of how these programs are set up aren't necessary to go into here.

What is important is how the F&I product provider can make these programs successful for the dealer. Our “secret” and the single most important factor that has made reinsurance programs so successful for the dealers who use our process can be described in one word...

...Penetrations!

Ad Loading...

Let me explain.

You see, as anyone involved in reinsurance knows, product penetrations control loss ratios. Take life insurance for instance. If the dealer only sells a few life policies every month, they don’t put away many reserves. So when the first customer the dealer sold a policy to dies, all of their meager reserves are sucked up and there's nothing left. These are called "shock losses" and they wipe out reserves very quickly. Also, if the dealer’s penetrations on life insurance are real low, they’re probably only selling life to people who feel they have a good chance of needing it. The same holds true with service contracts and other products that have risk attached.

To make any of these programs work, the dealer has to sell high penetrations of those products to people who won't have a claim to offset the ones who do.

Ironically, some agents and dealers sabotage their own reinsurance programs by trying to emphasize one product over the others. There are a lot of dealers I have worked with who have put too much emphasis on service contracts over other products to try to boost service contract penetrations with pay plans and spiffs, thereby, theoretically, lowering their exposure to claims. However, when they do that they don't really increase their service contract penetration to any meaningful degree, they just lose penetrations from other products that are not presented equally.

This point has been magnified in the past few years by the improper use of the old style four column menus that many companies sell and that are attached as a “bonus” to many of the tracking systems out there.

Ad Loading...

We developed every form of those menus in the early ‘90’s and we can make them work to some extent. But because of lack of training, or improper training, a tendency has evolved over time, in “real” F&I departments for the F&I manager to isolate on the last block on a single, (most important), product. Usually that was the service contract.

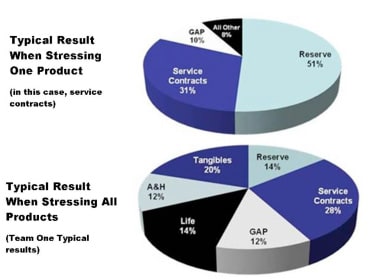

The examples below show the income distribution percentages from successful reinsurance dealers as opposed to those that have programs that do not perform as desired:

You see, to be successful in a reinsurance program, you have to sell all of your products to everybody, not just the ones who come in breathing with an Oxygen tank, or those who are skydiving instructors, or people buying 4 wheel drives.

The reason our F&I professionals have produced such successful reinsurance programs for their dealers is that they don't worry about the back end. They just concentrate on the overall success of the front end. Our most successful F&I departments also have the most profitable reinsurance programs.

I get a lot of positive feedback about our program from the agents who manage these programs because our process sells higher penetrations of all of the F&I products than any process in the marketplace. And I appreciate that.

Ad Loading...

However, we don't get those results because we manipulate the process to sell one product over another, but because we focus on selling all of the products to everyone. That's how our top performers do it and it's how our process is designed. Using the Package Option method has resulted in our dealers posting the lowest loss ratios in the industry as well as the highest income per unit.

Get your dealers to focus on maintaining top penetrations of all of their products the back end deals will take care of themselves. And you'll both make a lot more money. Guaranteed!

Forecasts show that the spring sales season is rising above overriding economic concerns, among them continuously rising car prices, trade tariffs, elevated interest rates, and now a war.

The Kerrigan Index shows that despite a chaotic year of musical trade tariffs, high vehicle prices and more roadblocks, acquirers still flush with pandemic-era cash accelerated the consolidation pace.

Labor shortages, material costs and tariffs are just a few of the reasons automakers are looking to expand their investments in automation and robotics this year.

The Middle East imports a sizable share of vehicles made in the states. It’s unclear how the Iran War could affect the keystone market for U.S. automakers.

Auto dealers don’t have to settle for high employee turnover. Despite historical patterns of rotating dealership doors, they can tweak their processes to find and keep the right people on staff.

New-vehicle sales fell year-over-year for the fifth month in a row in February, making retail deliveries the slowest they’ve been since 2023, according to a CarGurus report.

GM says it sells the cheapest electric vehicle in the U.S. market. It explains how it made improvements to the entry-level EV while keeping its price down.