Weekly Market Insights Report

The declines are continuing to close out the second week of 2022 with majority of segments reporting drops in valuations.

The declines are continuing to close out the second week of 2022 with majority of segments reporting drops in valuations.

BLACK BOOK – Wholesale Prices, Week Ending January 15th

The declines are continuing to close out the second week of 2022 with majority of segments reporting drops in valuations. The Van segments (Minivan, Compact, and Full-Size) continue to be the anomalies with values continuing to increase. Sales rates are improving compared to the end of 2021, but have not returned to pre-holiday levels.

This Week Last Week 2017-2019 Average (Same Week)

Car segments -0.19% -0.20% -0.60%

Truck & SUV segments -0.11% -0.13% -0.50%

Market -0.13% -0.15% -0.56%

Car Segments

On a volume-weighted basis, the overall Car segment decreased -0.19%. For reference, the previous week, cars decreased by -0.20%.

Eight of the nine Car segments declined last week. Sub-Compact Car reported a gain of +0.18%.

Premium Sporty Cars had the largest decline last week, at -0.35%.

Full-Size and Mid-Size Cars also had large decreases, -0.27% and -0.25%, respectively.

Truck / SUV Segments

The volume-weighted, overall Truck segment decreased -0.11%, compared to the prior week’s decrease of -0.13%.

Ten out of the thirteen Truck segments reported declines.

Compact Luxury and Mid-Size Luxury Crossovers had the largest declines last week, at -0.34% and -0.37%, respectively.

Full-Size Vans reported another week of gains, increasing +0.74%. This now marks the fiftieth increase in the last fifty-one weeks.

The other two van segments, Compact and Minivan, also reported increases of +0.94% and +0.08%, respectively.

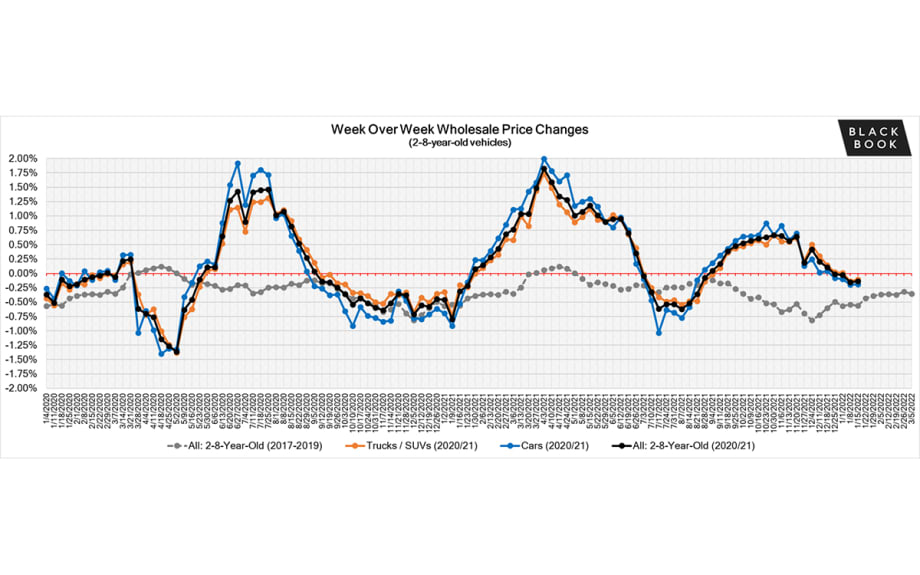

Weekly Wholesale Index

Calendar year 2020 and 2021 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 did not have typical seasonality patterns as the market has had rapid increases in wholesale values for the majority of the year, and the Wholesale Weekly Price Index reached the highest point of the year at the end of December, reporting at over 1.51 points. Now in calendar year 2022, the index has been reverted back to the 1.00 mark.

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year.

Retail (Used and New) Insights

Volkswagen’s all-electric van, the ID Buzz, finally has an official reveal date of March 9th. Unfortunately, we will have to wait until 18-to-24 months after the reveal to see them on sale.

The electric truck competition is hot, with Ford, GM, Rivian, and Tesla all bringing models to the market. We will have to wait a little longer for Tesla’s Cybertruck due to news that they will be delaying the start of production to the end of Q1 2023.

The chip shortage was the top automotive story of 2021, but has been quiet for 2022, so far. However, challenges are on the horizon with AutoForecast Solutions projecting global production to lose more than 800,000 units this year.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down at the end of 2020, and thus resulted in declining retail asking prices for the last several weeks of the year. As demand rebounded, retail prices lagged slightly behind wholesale prices, but March had an accelerated growth in retail prices. In April and May, retail prices picked up speed as demand accelerated, fueled by stimulus payments, tax season, and shortages of new inventory. During the third quarter, retail prices continued to rise at a slower rate but soon picked up the pace once again to start the fourth quarter. In Q4, prices on retail listings steadily increased week after week. As 2021 came to an end, the retail listing price index closed 36% above where the year began. In the first several weeks of 2022 the retail listing prices remain relatively unchanged as market seems to be in wait-and-see mode.

This analysis is based on approximately two million vehicles listed for sale on U.S. dealer lots. The graph below looks at 2-6-year-old vehicles.

Inventory

Used Retail

Used retail listings started off calendar year 2022 similar to calendar year 2021, with further declining used retail listings. With some forecasted improvements on the semiconductor front, hopefully the listings will increase as we go into the spring market with more trade-ins and rental returns.

Days-to-turn for used retail listings slightly increased over the last few months of 2021. Now in 2022, days-to-turn sits just above 38 days.

Wholesale

Availability of inventory remains a challenge in the wholesale channel, particularly quality units. However, most sellers are holding firm to the floors with hopes that the new year will bring back the return of increasing prices that were experienced throughout the majority of 2021. So far, we are seeing week-over-week value changes that are more typical of traditional seasonality expectations.

The weekly estimated average sales rate continues to improve, but not by much due to sellers holding firm on floors and scarce availability of quality units in the wholesale channel.

Originally posted on F&I and Showroom

More Sales

June Automotive Boon?

A forecast for this month’s new-vehicle sales tells a familiar 2026 story: Year-over-year comparisons must be made in light of last year’s aberrations.

Read More →

Affordable New Cars a Thing of the Past

More than one out of five new vehicles sell for more than $60,000, according to Edmunds. That's up 7% compared to prepandemic 2019.

Read More →

Legacy Automakers Risk Falling Behind

As legacy automakers, mostly in the U.S. and Japan, have revised their 2030 electric-vehicle sales targets and shifted to a hybrid focus, they risk falling behind new market leaders.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

New Vehicles Down for Most Brands

Healthy May sales cut into inventory as automakers kept a tight reign on supply, though some brands ended the month with excess units on the ground.

Read More →

New-Car Demand on the Rise

For the first time this year, new-vehicle demand rose in May, up nearly 6% year-over-year, according to CarGurus’ Intelligence Report.

Read More →

Auto Prices Ride May Moderation

Flat ATPs and asking prices clocked in below long-term averages for the month, though some segments saw significant price gains, reported Cox Automotive.

Read More →

Nissan Reports Significant Sales Growth

Following the release of Nissan’s 2025 fiscal year report, the automaker announced that its retail-first approach has led to a significant jump in dealer sales.

Read More →

Inventory of New Units Stable

Auto brands spent April clearing out most of their 2025 supply with incentives while holding firm on 2026 prices, striking a balance to meet demand and protect their bottom lines.

Read More →

The Hidden Edge

Reflections from the 2026 Agent Summit: gratitude, gut decisions, and the power of the first contact

Read More →