Market Insights from Black Book

On a volume-weighted basis, the overall Car segment increased +0.18%. For reference, the previous week cars increased by +0.06%.

On a volume-weighted basis, the overall Car segment increased +0.18%. For reference, the previous week cars increased by +0.06%.

BLACK BOOK – Wholesale Prices, Week Ending September 4th

Positive gains continued last week, with 15 of the 22 vehicle segments reporting increases. Wholesale prices are expected to continue to trend upward as new and used inventory remains constrained in addition to the damages of hurricane Ida that caused catastrophic flooding in Louisiana and in the Northeast last week.

This Week Last Week 2017-2019 Average (Same Week)

Car segments +0.18% +0.06% -0.11%

Truck & SUV segments -0.02% -0.14% -0.12%

Market 0.04% -0.07% -0.12%

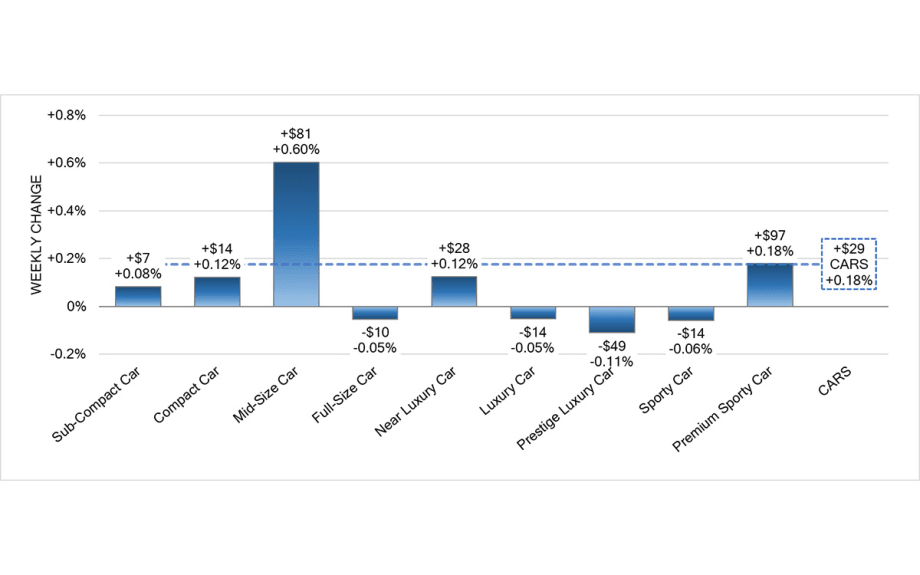

Car Segments

On a volume-weighted basis, the overall Car segment increased +0.18%. For reference, the previous week cars increased by +0.06%.

Five of the nine car segments reported gains last week, with Mid-Size Cars (+0.60%) increasing by the largest amount.

Compact Cars (+0.12%) increased for the third week in a row for an average weekly increase of (+0.17%).

Near Luxury Cars had nine weeks of declines but moved back into positive territory last week, with an increase of +0.12%.

Truck / SUV Segments

The volume-weighted, overall Truck segment declined -0.02%, less than the previous week’s decline of -0.14%.

The largest volume segments, Full-Size Trucks (-0.51%) and Mid-Size Crossovers (-0.13%) experienced declines this past week, which led to the overall Truck segment reporting minimal declines.

Full-Size Vans increased +1.25%, compared to the prior week’s increase of +0.83%. The segment has now had 31 of the last 32 weeks reporting increases for an average weekly increase of +0.55%.

Weekly Wholesale Index

Calendar year 2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 has not had typical seasonality patterns as the market has had rapid increases in wholesale values for the majority of the year. After reaching record heights at the end of June, wholesale prices began to decline at a rate higher than the typical seasonal decline. As we move into the Fall season, wholesale prices are beginning to show positive movement once again.

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year.

Retail (Used and New) Insights

August new car sales were down 17% due to the continued microchip shortage depleting dealer’s inventory. Ford, Toyota, and Honda all reported declines in sales.

Ford is facing more downtime and reduced shifts at multiple facilities that are responsible for full-size truck and SUV production. The facility in Kansas that produces the F-150 has already been down for two weeks and will be closed for an additional week due to the lack of microchips.

In recent weeks, Toyota, Volkswagen, Honda, and more have announced their expectation for September production to be significantly impacted by the microchip shortage. Mercedes-Benz is the latest in the string of announcements to warn that their Q3 sales will be impacted due to the downtime spawning from the shortage.

Genesis is transitioning their line-up away from ICE to BEVs and fuel-cells. Their line-up is slated to be all-electric by 2025 and they set a goal of tripling their global sales by this date.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down at the end of last year, and thus resulted in declining retail asking prices for the last several weeks of 2020. As demand rebounded, retail prices have lagged slightly behind wholesale prices, but March had an accelerated growth in retail prices. In April and May, retail prices picked up speed as demand accelerated, fueled by stimulus payments, tax season, and shortages of new inventory. In June, retail prices continued to rise. After strong Spring and Summer months, retail listing prices seemed to stabilize at a level more than 24% above where we started the year.

This analysis is based on approximately two million vehicles listed for sale on US dealer lots. The graph below looks at 2-6-year-old vehicles.

Inventory

Used Retail

Current used retail listing volume is about 14% below the start of the year. Used inventory is now starting to decrease again due to a slowdown of trade-ins and lease returns.

Days-to-turn for used retail listings have been increasing, as retail demand softened over the last few weeks. The days-to-turn now sits just above 34 days, which is still lower than what is typically expected in a normal year.

Wholesale

Sales rates declined slightly last week, as sellers held firm to floors. However, heading into this week, we are expecting improved sales rates as dealers prepare for increased demand as a result of the flooding in Louisiana and the Northeast due to hurricane Ida.

Newer used units are seeing considerable strength as they provide dealers with new car substitutes for their customers. The overall wholesale market for 2-8-year-old vehicles increased by 0.04% last week, but 0-2-year-old increased +0.25%.

Originally posted on Auto Dealer Today

More Sales

June Automotive Boon?

A forecast for this month’s new-vehicle sales tells a familiar 2026 story: Year-over-year comparisons must be made in light of last year’s aberrations.

Read More →

Affordable New Cars a Thing of the Past

More than one out of five new vehicles sell for more than $60,000, according to Edmunds. That's up 7% compared to prepandemic 2019.

Read More →

Legacy Automakers Risk Falling Behind

As legacy automakers, mostly in the U.S. and Japan, have revised their 2030 electric-vehicle sales targets and shifted to a hybrid focus, they risk falling behind new market leaders.

Read More →

New Cars a Tad More Affordable

May averages show that combined circumstances gave auto consumers slightly better buying power for the month, though average prices were up year-over-year.

Read More →

New Vehicles Down for Most Brands

Healthy May sales cut into inventory as automakers kept a tight reign on supply, though some brands ended the month with excess units on the ground.

Read More →

New-Car Demand on the Rise

For the first time this year, new-vehicle demand rose in May, up nearly 6% year-over-year, according to CarGurus’ Intelligence Report.

Read More →

Auto Prices Ride May Moderation

Flat ATPs and asking prices clocked in below long-term averages for the month, though some segments saw significant price gains, reported Cox Automotive.

Read More →

Nissan Reports Significant Sales Growth

Following the release of Nissan’s 2025 fiscal year report, the automaker announced that its retail-first approach has led to a significant jump in dealer sales.

Read More →

Inventory of New Units Stable

Auto brands spent April clearing out most of their 2025 supply with incentives while holding firm on 2026 prices, striking a balance to meet demand and protect their bottom lines.

Read More →

The Hidden Edge

Reflections from the 2026 Agent Summit: gratitude, gut decisions, and the power of the first contact

Read More →