Shortcuts and Compliance Are Not Friends

Don’t let process shortcuts short-circuit all the hard work your dealer has put in to make their dealership the success it is today.

Don’t let process shortcuts short-circuit all the hard work your dealer has put in to make their dealership the success it is today.

IMAGE: Pixabay

Once upon a time, I was part of corporate America while working for one of the captives. While in corporate America, I had an accident with my right hand, which ended up requiring a cast. I couldn’t grab the steering wheel with my right hand, my putter grip was abysmal, and I couldn’t write or sign my name.

As a supervisor in my branch office, I was responsible for completing a checklist on every repossessed account to ensure all the required steps from repossession to disposal had been completed.

I had to initial a box by each completed task to properly finish the checklist. Since I couldn’t drive, putt, or write, I just assumed my boss would understand if I marked a simple checkmark in each box. I evidently didn’t know my boss very well. “Shortcuts are not acceptable!” he bellowed when he reviewed the first of a stack of repossessions I had completed.

I assume shortcuts develop in many industries, companies, or processes. Some of the shortcuts I witness in dealerships create potential compliance concerns. As a trusted advisor to your dealer clients, you should be on the lookout for these shortcuts and discuss the potential risk with them.

Handwriting Product

Pricing In a perfect world, the customer signs at least three documents disclosing the acceptance and pricing of voluntary protection products: menu, buyer’s order (or PCD in California), RISC/lease, and enrollment form. There are times when the product price does not print on the enrollment form, instead it is either left blank or prints as “N/A.” Other times, the dealer management system (DMS) picks up the wrong price, perhaps printing the price of the vehicle service contract on the maintenance form.

The form in the file either reflects the free price (blank or N/A) or the wrong price, or the correct price that has been handwritten in. Oftentimes, when the price is corrected, the customer has not initialed the change. This begs the question, exactly what does the customer’s copy show?

Hopefully, the customer’s copy is consistent with the dealer’s copy, otherwise there could be some explaining to do if the customer ever decides to file a complaint or litigation and the file is requested in discovery.

Taking the shortcut to not having the DMS corrected or programmed or not properly loading the deal is potentially putting the validity of the transaction at risk.

Used Car Buyer’s Guide Disclosure

The FTC Used Car Rule is very specific about the language that must be used to properly disclose any remaining warranty. Most dealers have a solid process to properly make this disclosure. For example, the Used Car Rule says that using shorthand terms such as “factory warranty remaining” is not a sufficient disclosure. The vendors who manage the buyer’s guide process for dealers generally have the correct, safe-harbor language.

The process falls apart when a used vehicle is sold before the vendor has an opportunity to put a correct buyer’s guide on the vehicle. Sometimes it falls apart when the salesperson gets lazy and handwrites a buyer’s guide instead of taking the guide off of the vehicle or printing one from the dealer’s software. Going the shortcut route thinking you are saving time leads to non-compliance with a federal law.

Signing Customer Names

People get busy. Salespeople fail to get the customer’s signature on the privacy notice, or F&I managers forget to have the customer sign the gap enrollment form.

Almost every dealership employee understands that forging a customer’s signature to a form is a crime. Others rationalize that the customer did agree or knew that they agreed to the privacy policy or signed a menu and contract agreeing to purchase GAP, so it is all right to sign their name.

Forging a customer’s name is never an acceptable shortcut.

Not Reviewing the Buyer’s Order/RISC

During your next managers sales meeting, ask how many of your managers have read and understand each section, front and back, of the buyer’s order, the retail installment sales contract, and the lease agreement. After all, they are likely signing these documents on behalf of the dealership. Isn’t it reasonable to expect that they have read and understand all the provisions they are asking customers to agree to?

Sometimes a shortcut is just being lazy instead of understanding the very basics of your job. Don’t let process shortcuts short-circuit all the hard work your dealer has put in to make it the success it is today.

Continued good health and good selling.

More Industry

Pennsylvania Dealership Under New Retailers

The sale of the Chrysler Dodge Jeep Ram store puts a family auto group on a leaner path as first-time dealers take the helm.

Read More →

Battery Storage Takes Priority Over EVs

U.S. automakers are prioritizing battery energy stationary storage over electric-vehicle production as the consumer demand for EVs lags the rest of the world.

Read More →

Auto Dealers Feel Better But Not Great

A second-quarter Cox Automotive poll of franchised retailers and independents found better views of the current market after a good spring but anticipation of third-quarter storminess.

Read More →

New-Vehicle Sales Picture Relative

A May forecast is complicated by last spring’s trade tariff effects on auto retail. Despite continued hard realities, many consumers took advantage of ways to bite the bullet.

Read More →Auto Group Acquires Third Nissan Rooftop

Iowa-based Coleman Automotive Group recently acquired its seventh dealership, McGrath Nissan, which it renamed Nissan of Elgin.

Read More →

April Less Affordable

Based on prices, reduced incentives and slower household income growth, consumers found it more challenging to buy new last month, Cox Automotive reported.

Read More →

Building an Extraordinary F&I Agency

Work to determine your specialized talent, because that fact will determine everything about your agency’s future.

Read More →

Recipe for Compliance

The secret to both amazing barbecue and compliance is the same: understanding the basics and committing to a process.

Read More →

EVs Getting More Attractive

A growing percentage of U.S. consumers are open to switching and fewer are adverse to the idea, according to a recently completed survey. That’s despite the end of a tax break.

Read More →

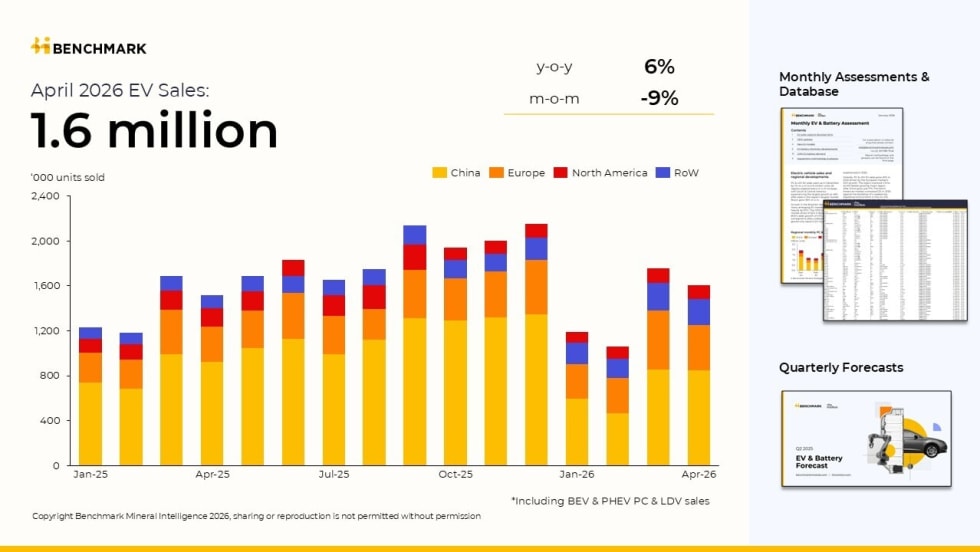

EV Sales Drop in April Following Surge

North American electric-vehicle sales were down 28% year-over-year, a sharp contrast from global EV sales growth of 6%.

Read More →