Black Book: Weekly Market Insights

New inventory is not expected to see improvement until the third quarter of this year, so values are expected to remain at elevated levels throughout the summer.

New inventory is not expected to see improvement until the third quarter of this year, so values are expected to remain at elevated levels throughout the summer.

Wholesale Prices, Week Ending May 15th

The week-over-week increases continued for a sixteenth consecutive week. With the availability of used and new inventory remaining low, the values continue to push higher. New inventory is not expected to see improvement until the third quarter of this year, so values are expected to remain at elevated levels throughout the summer.

Car Segments

Car segment gains ticked up slightly this past week (+1.30%) compared to the week prior (+1.25%).

Seven of the nine car segments had gains exceeding +1.00%.

Compact Cars are no longer experiencing weekly gains exceeding 2%, but the nine-week average increase is +2.04%.

For the first time since mid-March, the Sub-Compact Car segment had increases below 1%.

Near Luxury Car increased the rate of gains this past week (+1.22%), compared to the prior week (+1.04%).

Sporty Cars continue to see large gains (+1.24%), compared to +0.36% during this same week in 2019.

Truck Segments

Truck segment gains increased this past week (+1.12) compared to the previous week (+0.98%).

All thirteen truck segments reported gains last week, with six exceeding +1.00%.

Compact Crossovers led the gains at +1.86% this past week. In comparison, this same week in 2019, the segment showed a decline of -0.08%.

Most of the Luxury segments have seen value increases decline in magnitude, but compared to 2019, all of these segments were experiencing declining values. For example, Full-Size Luxury declined by -0.59% during this same week in 2019.

Newer Used Vehicles (0-2-year-old)

Driven by an extreme shortage of rental returns and limited inventory of new vehicles, the price trends of newer used vehicles have been experiencing larger weekly gains compared to the older units. Within the last three weeks, newer used units reached levels that, in some cases, exceed new car pricing while the rate of growth has slowed for older units. For example, in addition to F150 Raptor, 2020-21 Chevrolet Corvette, and 2021 Jeep Gladiator and Wrangler, dealers are paying above MSRP for 2021 Kia Telluride and Hyundai Palisade, as well as other mainstream models.

The table below shows the average weekly price changes for 0-2-year-old vehicles.

Weekly Wholesale Index

2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g. 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. It is now clear that 2021 will also not have typical seasonality patterns as the market is going through a rapid increase in wholesale values. The spring market arrived about 7 weeks earlier and with much stronger price increases compared to a typical pre-COVID year. The graph below looks at trends in wholesale prices of 2-6-year old vehicles, indexed to the first week of the year. Currently, wholesale prices are more than 27% higher compared to the beginning of the year (adjusted for the mix).

Retail (Used and New) Insights

General Motors announced price increases on their 2021 GMC line-up with most of the increases ranging from $50 to $800 to be applied to the base MSRP.

Electrification is in the plans for the majority of OEMs now with major announcements coming out every few weeks about new models to come:

On May 19th, Ford will unveil their electric Full-Size Pickup, to be called F-150 Lightning.

Porsche announced their plans to release an all-electric Macan variant in 2023, after a refreshed gasoline powered Macan will be released in 2022.

The global microchip shortage continues to wreak havoc on production levels. Nissan announced they are expecting to see a reduction of 500,000 units in 2021.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down at the end of last year, and thus resulted in declining retail asking prices over the last several weeks of 2020. As demand rebounded in January, retail prices seemed to lag wholesale prices – retail asking prices continued to decline throughout January and remained stable in February. March had an accelerated growth in retail prices, but the rate of growth is still lower compared to the increases of wholesale prices. In April, retail prices picked up speed as demand accelerated, fueled by stimulus payments, tax season, and shortages of new inventory. Currently, the prices are more than 15% above where we started the year.

This analysis is based on approximately two million vehicles listed for sale on US dealer lots. The graph below looks at 2-6-year-old vehicles.

Volume

Used Retail

Current used retail listing volume is about 14% below the start of the year, but the inventory levels stabilized in the last 4 weeks.

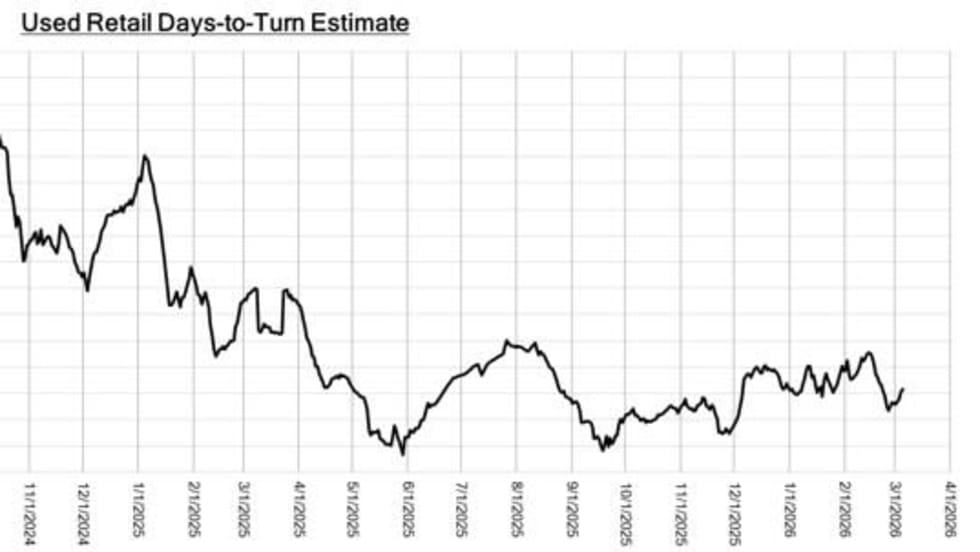

Days-to-turn have been decreasing since the middle of March, as retail demand picked up across the country due to tax returns and the additional round of $1,400 stimulus checks deposited into consumers’ bank accounts.

Wholesale

Floor pricing continues to increase each week, but availability of average and clean units remains scarce which is leading to declining conversion rates in recent weeks.

Despite the limited inventory on dealer lots, many dealers are finding themselves receiving greater profit margins in the wholesale channel as opposed to their own retail lots.

Armed with the knowledge that their available inventory in the pipeline is extremely limited, remarketers are finding that they are able to continue to raise their floors and hold firm on their set values. They plan to accept a no-sale this week with the expectation it will sell the next.

Originally posted on F&I and Showroom

More Sales

Nissan Reports Significant Sales Growth

Following the release of Nissan’s 2025 fiscal year report, the automaker announced that its retail-first approach has led to a significant jump in dealer sales.

Read More →

Inventory of New Units Stable

Auto brands spent April clearing out most of their 2025 supply with incentives while holding firm on 2026 prices, striking a balance to meet demand and protect their bottom lines.

Read More →

The Hidden Edge

Reflections from the 2026 Agent Summit: gratitude, gut decisions, and the power of the first contact

Read More →

March New-Vehicle Sales Don’t Reflect War

Cox Automotive data shows Americans doubled down on big-is-better despite price increases. Slightly higher incentives helped fuel the demand.

Read More →

Service Drives Gen Z Loyalty

The dealership profit center plays an important role in customer retention, and generation Z customers are showing the highest loyalty rates, based on recent CDK Global data.

Read More →

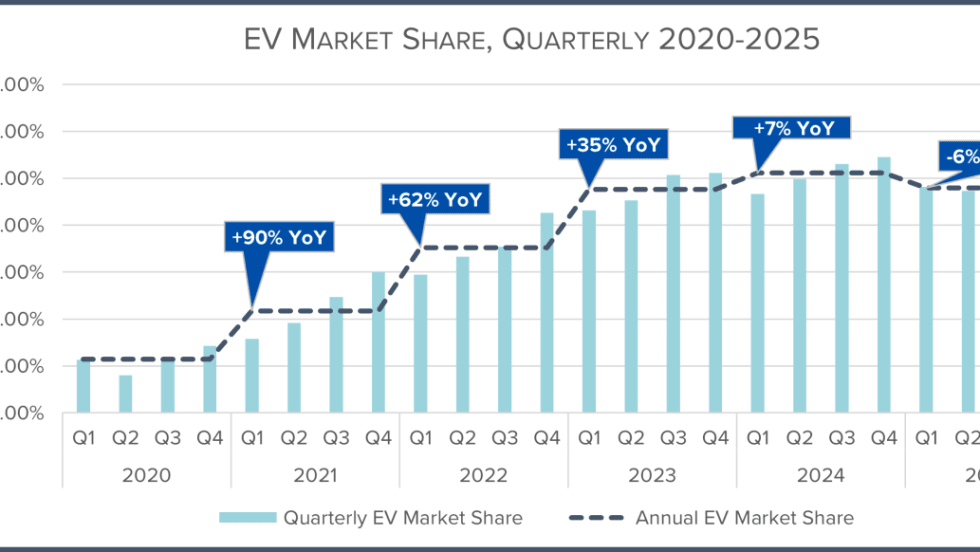

EV Sales Slide While Hybrids Climb

California, as usual, led the country in EV registrations in the fourth quarter, but the U.S. as a whole saw a 43% year-over-year volume decrease.

Read More →

Lease Buyouts Deemed Favorable

Better financing conditions and the potential to save money on monthly payments could drive more consumers to buy out their vehicle leases instead of opting for a new lease payment.

Read More →

Black Book: Weekly Market Update

Both vehicle values and conversion rates sped up last week as two segments outperformed in the pre-spring burst of buying.

Read More →

Used-Vehicle Program Aims to Draw More Buyers

GM says more than 750 dealers across the U.S. are enrolled in CarBravo and that in January CarBravo dealers sold over two times the certified volume of Chevrolet, Buick and GMC dealers using traditional CPO.

Read More →

Creating Agency Loyalty

There are tried and true ways to instill it while also protecting your agency from competitors and other roadblocks.

Read More →