Market Insights Report

Black Book recently published an update to their weekly Market Insights report.

Black Book recently published an update to their weekly Market Insights report.

IMAGE: Black Book

BLACK BOOK – We recently published an update to our Weekly Market Update.

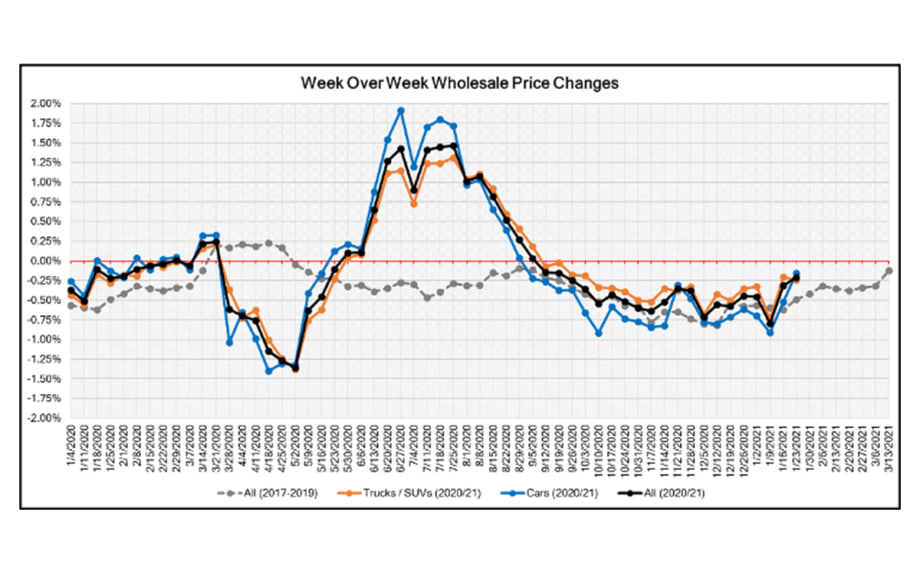

Wholesale Prices

Wholesale prices continued their decline last week for the twentieth week in a row. Volume-weighted, overall Car and Truck segments both experienced continued softening in values last week, with the overall rate of decline decreasing compared to recent weeks.

This Week Last Week Historical Average

Car segments. -0.16%. -0.52% -0.49%

Truck & SUV segments. -0.24%. -0.20% -0.39%

Market -0.21% -0.31% -0.44%

Car Segments

Sub-Compact and Compact Car segments reversed direction after 21 weeks of declines this past week, with both segments experiencing week-over-week gains in value.

The volume of off-lease 2018 model year Near Luxury and Luxury Car models has been increasing in recent weeks and this is reflected in their recent price trend, a decline of -0.42% and -0.38%, respectively.

Sporty Cars are starting to show signs of the spring market on the horizon with their weekly depreciation rate slowing from 0.29% a few weeks ago to 0.08% this past week.

Truck Segments

Full-Size SUVs increased for a third week in a row at 0.05%, due to low new inventory continuing to drive the demand for used units that are also in short supply.

Full-Size Trucks had fifteen weeks of softening values, but this past week they stabilized. Despite the consecutive weeks of declines, the Full-Size Truck segment finished out 2020 with values up 8.7%.

Minivans took the top spot for the largest declining Truck segment for multiple weeks during the fourth quarter of 2020, but 2021 is bringing on a new trend. The past two weeks the Minivan segment has seen weekly depreciations below 0.30%.

Weekly Wholesale Index

2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g. 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. The question still remains whether we will go back to normal seasonality in 2021.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down leading up to the December holidays, and thus resulted in declining retail asking prices over the last several weeks of 2020. Retail prices recently started to increase as retail demand has begun to increase.

Days-to-turn have been increasing since November but remain at levels below average. Recent increases in retail demand are expected to keep the days-to-turn below average in Q1.

Retail (Used and New) Insights

Dealers continue to report an uptick in used retail sales, particularly when compared to a typical January, and some dealers are now attributing the uptick to the $600 stimulus that came at the end of 2020. New retail demand is also still doing well, but dealers are reporting a slowdown in activity compared to December.

The global shortage of microchips continues to ripple through the automotive industry with a majority of the OEMs being impacted in some capacity and having to alter their production plans as a result of the COVID-19 induced shortage. Last week, GM announced the impact on their recently redesigned full-size SUV line-up.

Ford announced they are recalling 3 million vehicles due to a potential airbag inflator defect at a cost of $610 million.

It is now official that PSA Group and Fiat Chrysler Automobiles have merged to become Stellantis. This makes the newly created company the fourth largest automaker in the world. The new company represents 14 brands globally: Chrysler, Dodge, Jeep, Ram, Fiat, Alfa Romeo, Abarth, Lancia, and Maserati, from FCA, are now jointed by Citroën, DS, Opel, Peugeot, and Vauxhall, from PSA.

Volume

Used Retail

Used retail listing volume stayed essentially flat since the beginning of the year but remains at levels above where the industry was in January, during the pre-COVID time of 2019.

Wholesale

Sales rates remain above December levels as dealers are optimistic about increased used demand fueled by continued low new inventory levels, stimulus payments, and the potential of a traditional Spring/tax season.

Uncertainty remains around the future of a traditional spring/tax season market. Early sentiments by dealers are optimistic and auction performance of the traditional spring market vehicles, those under $12,000, have seen an uptick in demand in the last few weeks.

Wholesale volume has shown improvement in recent weeks, especially with 2018 model year vehicles now coming off-lease. However, remarketers are still reporting lower than normal levels of volume in the pipeline for Q1.

Originally posted on Auto Dealer Today

More Sales

Nissan Reports Significant Sales Growth

Following the release of Nissan’s 2025 fiscal year report, the automaker announced that its retail-first approach has led to a significant jump in dealer sales.

Read More →

Inventory of New Units Stable

Auto brands spent April clearing out most of their 2025 supply with incentives while holding firm on 2026 prices, striking a balance to meet demand and protect their bottom lines.

Read More →

The Hidden Edge

Reflections from the 2026 Agent Summit: gratitude, gut decisions, and the power of the first contact

Read More →

March New-Vehicle Sales Don’t Reflect War

Cox Automotive data shows Americans doubled down on big-is-better despite price increases. Slightly higher incentives helped fuel the demand.

Read More →

Service Drives Gen Z Loyalty

The dealership profit center plays an important role in customer retention, and generation Z customers are showing the highest loyalty rates, based on recent CDK Global data.

Read More →

EV Sales Slide While Hybrids Climb

California, as usual, led the country in EV registrations in the fourth quarter, but the U.S. as a whole saw a 43% year-over-year volume decrease.

Read More →

Lease Buyouts Deemed Favorable

Better financing conditions and the potential to save money on monthly payments could drive more consumers to buy out their vehicle leases instead of opting for a new lease payment.

Read More →

Black Book: Weekly Market Update

Both vehicle values and conversion rates sped up last week as two segments outperformed in the pre-spring burst of buying.

Read More →

Used-Vehicle Program Aims to Draw More Buyers

GM says more than 750 dealers across the U.S. are enrolled in CarBravo and that in January CarBravo dealers sold over two times the certified volume of Chevrolet, Buick and GMC dealers using traditional CPO.

Read More →

Creating Agency Loyalty

There are tried and true ways to instill it while also protecting your agency from competitors and other roadblocks.

Read More →